Are Tradeline Companies Legit? | Last Updated: July 2026 | Author: CPN Tradelines Team | Reading Time: 8 min

Are tradeline companies legit? Yes — but not all of them, and that distinction matters more than most people realize before they spend money. The practice of authorized user tradelines is completely legal and has been around for decades. The companies that sell them, however, range from highly professional operations with vetted accounts and clear processes to fly-by-night outfits that collect payment and disappear. This guide tells you exactly how to tell the difference.

What You Will Learn in This Guide

- Whether tradeline companies are legit and what the law actually says

- How to tell a legitimate company from one that isn’t

- What red flags signal a company is not worth your time or money

- What legitimate tradeline companies do differently

- Frequently asked questions about tradeline company legitimacy

Are Tradeline Companies Legit? What the Law Actually Says

Let’s start here because this is where most of the confusion lives. The practice itself — adding someone as an authorized user to a credit account so they benefit from its reporting history — is explicitly legal under the Equal Credit Opportunity Act (ECOA) and Regulation B. These laws require credit bureaus to include authorized user account history in personal credit reports. The Federal Reserve Board confirmed this requirement in its Regulation B regulatory commentary.

This is not a loophole or a gray area. It’s the same mechanism families have used for decades — parents adding children to accounts, spouses sharing established credit histories. The commercial tradeline industry applies the same legal framework in a professional, structured context.

So are tradeline companies legit as a category? Yes. Are every tradeline company and every practice within the industry operating legitimately? That’s a different question — and that’s what the rest of this guide addresses.

Are Tradeline Companies Legit — How to Tell the Difference

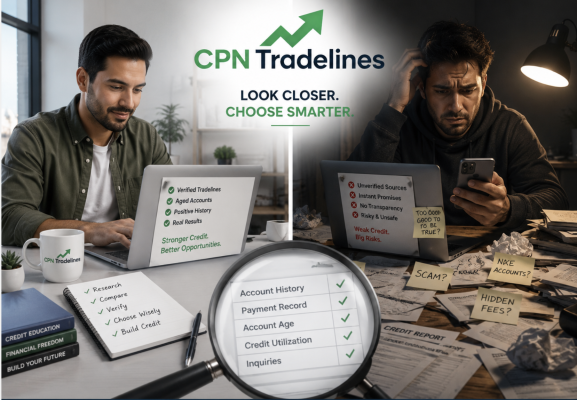

The legitimacy question isn’t really about the practice — it’s about the company. Here’s what separates reputable tradeline operations from ones that aren’t worth your money or your trust:

They’re transparent about account details before you pay. A legitimate tradeline company tells you the exact age, credit limit, payment history, current balance, and bureau reporting for every account before you commit a dollar. If they’re vague about specifics or say they’ll share details after payment, that’s not a company operating in good faith.

They verify account quality before client placement. Every account should have zero late payments ever. One 30-day late mark on a tradeline you’re added to can hurt your score rather than help it. Reputable companies check this before placement — not after a client complains.

They give honest timeline expectations. Legitimate companies tell you tradelines typically post within 30 to 45 days depending on the card issuer’s billing cycle. Anyone promising results in 24 to 48 hours or guaranteeing a specific score increase is not being straight with you.

They have a clear policy if something goes wrong. Posting delays happen. Card issuers change billing cycles, bureaus have processing backlogs. A legitimate company has a written refund or replacement policy for situations where a tradeline doesn’t post as expected. No policy means no recourse.

They’ve been around long enough to have a track record. Verifiable years in business, third-party reviews outside their own website, and the ability to answer specific questions about their process — these are the markers of an operation that has been doing this long enough to know what they’re doing.

Signs a Tradeline Company Is NOT Legit

These are the warning signs worth knowing before you hand over money to anyone:

| Red Flag | What It Usually Means |

|---|---|

| Guaranteed score increases of a specific number | No legitimate company can guarantee results — results vary by profile and account quality |

| No refund or replacement policy | They have no process for accountability when things go wrong |

| Won’t disclose account age, limit, or payment history before payment | They either don’t have that information or don’t want you evaluating it before committing |

| Pressure to decide immediately — “limited availability” | A manufactured urgency tactic, not a genuine constraint |

| No verifiable business history or third-party reviews | New operation with no track record — or one that keeps rebranding after complaints |

| Prices dramatically lower than the market | Lower-quality accounts, unverified payment histories, or accounts that may not post |

What Legitimate Tradeline Companies Look Like

Here’s what you should be able to verify before committing to any provider:

| Standard | What a Legitimate Company Does |

|---|---|

| Account disclosure | Provides exact age, limit, balance, payment history, and bureau reporting before purchase |

| Account verification | Confirms zero late payments on every account before any client placement |

| Timeline honesty | States realistic 30 to 45 day posting window without overpromising |

| Post-placement follow-up | Monitors that the tradeline posted correctly and addresses issues proactively |

| Written policies | Has a documented refund or replacement process for accounts that fail to post |

| Verifiable history | Years in business, third-party reviews, accessible team that answers specific questions |

Are Tradeline Companies Legit for Building Real Credit?

This is the deeper version of the legitimacy question — not just “is this legal” but “does it actually work.” The answer is yes, when the right conditions are met.

When you are added to a well-maintained account as an authorized user, that account’s history reports on your credit file through Experian, Equifax, and TransUnion exactly as if you had always held that account. The FICO scoring model treats authorized user account history the same as primary account history for scoring purposes. The result — a potentially significant score improvement within one to two billing cycles — is real and documented.

What doesn’t work is a low-quality account from a company that hasn’t verified it properly. An account with hidden late payments, high utilization, or bureau reporting gaps produces nothing at best and a score drop at worst. That’s why the company matters as much as the practice.

What Realistic Results Look Like

To answer whether tradeline companies are legit in terms of actual outcomes, here’s what clients across different starting profiles consistently experience:

| Starting Profile | Typical Score Improvement | Timeline |

|---|---|---|

| No credit history (thin file) | 60 to 120 points | 1 to 2 billing cycles |

| Fair credit (580 to 669) | 30 to 80 points | 1 to 2 billing cycles |

| Damaged credit (collections, lates) | 20 to 50 points | 1 to 2 billing cycles |

| Good credit (670 to 739) | 10 to 30 points | 1 to 2 billing cycles |

These are real ranges based on real outcomes — not guarantees, not worst-case scenarios. The thin-file numbers are the most dramatic because scoring models have so little data to calculate from that adding a seasoned account fundamentally changes what they can produce.

Why We Think This Question Matters

People searching “are tradeline companies legit” are usually doing so because they got burned once, heard a bad story, or are being appropriately cautious before spending money on something they don’t fully understand yet. All of those are good reasons to ask the question.

The honest answer is that the industry has legitimate players and illegitimate ones — just like credit repair, financial advising, or any other service industry that operates in a space where consumers are vulnerable. The answer to the legitimacy question depends entirely on which company you’re evaluating.

We have been doing this since 2006. Our accounts are verified before every placement. Our clients know the exact age, limit, and payment history of what they’re being added to before a dollar changes hands. And we have a clear process for the rare situations where something doesn’t go as planned. That’s what legitimacy looks like in practice — not just claiming it.

Frequently Asked Questions

Are tradeline companies legit or is this a scam?

The practice is completely legal under the Equal Credit Opportunity Act and Regulation B. Legitimate companies operating within this legal framework are not scams. The risk is in choosing a provider that doesn’t vet account quality, doesn’t disclose details before payment, or has no accountability process when things go wrong.

Can a tradeline company get me in legal trouble?

Being added as an authorized user to a credit account is not illegal and carries no legal risk to you. The legal issues in the credit space arise from different activities entirely — such as using false identification on credit applications. Authorized user tradelines from a reputable company carry no such risk.

How do I verify a tradeline company is legitimate before paying?

Ask for the exact age, credit limit, payment history, and bureau reporting for the specific account before committing. Check for third-party reviews outside the company’s own website. Ask about their policy if the tradeline doesn’t post. A company that answers these questions clearly and without pressure is operating legitimately.

Are tradeline companies legit for business credit too?

Yes. Business tradelines operate through a separate reporting ecosystem — Dun & Bradstreet, Experian Business, and Equifax Business rather than personal bureaus — but the same legitimacy standards apply. Verify account details upfront, confirm the accounts report to the bureaus that matter for your financing goals, and work with a provider that has a track record in business credit specifically.

How long does it take to see results from a legitimate tradeline company?

Most tradelines post within 30 to 45 days of placement, depending on the card issuer’s billing cycle. You can verify the tradeline posted correctly by checking your reports through AnnualCreditReport.com approximately 30 to 45 days after being added.

What should I do if a tradeline company doesn’t deliver?

First, check your reports at all three bureaus — sometimes a tradeline posts to one but not others, or posts slightly outside the expected window. If it genuinely didn’t post, contact the company and ask about their replacement or refund policy. A legitimate company will have a process for this. One that doesn’t have a clear response is telling you something important about how they operate.

The Bottom Line — Are Tradeline Companies Legit?

Yes — the practice is legal, the results are real, and reputable companies operate transparently within a well-established legal framework. The question worth asking isn’t whether tradeline companies are legit as a category. It’s whether the specific company you’re considering is operating with the account quality, the transparency, and the accountability that the legitimate ones do.

Ask the right questions before you pay. Verify the details. Check the track record. And if a company can’t or won’t answer your questions clearly — that’s your answer right there.

Ready to Work With a Tradeline Company That Can Actually Back It Up?

We have been placing clients on verified, high-quality tradelines since 2006. Every account in our inventory is checked before placement. Every client knows exactly what they’re getting before they commit.

Request Your Free Consultation — cpntradelines.com/contact-us/

No cost. No hard credit pull. No pressure — just straight answers from a team with a two-decade track record.

About CPN Tradelines

CPN Tradelines has specialized in credit profile strategy since 2006, working with clients across all 50 states. We help individuals and business owners build real, lasting credit using legal, transparent methods — and we answer every question before you commit to anything.